How to Pay Off Debt Using the Debt Snowball Method

If you’ve ever felt like your debt is going to go with you to the grave, you may change your mind once you learn about the Debt Snowball Method of paying off debt.

If you are facing a mountain of debt, like I once was (six figures of student loan debt totaling $105K) you may wonder if you’ll ever be able to pay it off. You might even feel it’s impossible, so what’s the point in even trying?

This is exactly how I felt when I first began my debt free journey. Overwhelmed. Hopeless. In fact, I put off even attempting to pay off my $105K in student loan debt for YEARS, because I just didn’t think it was possible. Surely no one can pay off THAT MUCH DEBT, right? Wrong. It can be done. And the Debt Snowball Method is a great way to start for beginners.

In this article, I’ll guide you step-by-step through starting your own Debt Snowball.

What is the Debt Snowball?

With the Debt Snowball, you pay off your debts from smallest to largest. You simply list all your debts, by total amount owed, from smallest to largest. You pay minimums on all your debts. Then, you throw every extra penny you can find at the smallest debt. Once that debt is paid off, you take the amount you were sending to that debt (minimum + extra), and throw it at the second debt.

As you keep going, the amount you are sending to each debt gets bigger and bigger, much like rolling a snowball downhill or around in the backyard.

With the Debt Snowball, you pay off your debts from smallest to largest.

The idea is that once you pay the small ones off, you get a series of quick wins that builds momentum to keep the debt pay-off going strong.

The momentum of the snowball as it grows over time makes it easier and faster to pay off debt as you continue this method.

Plus, the series of wins you get in the beginning encourages you to stay on track. This is a great method to use at any time, but especially if you are new to paying off debt.

How to Start Your Own Debt Snowball

I’ll walk you through the steps of starting your own debt snowball. It’s easy!

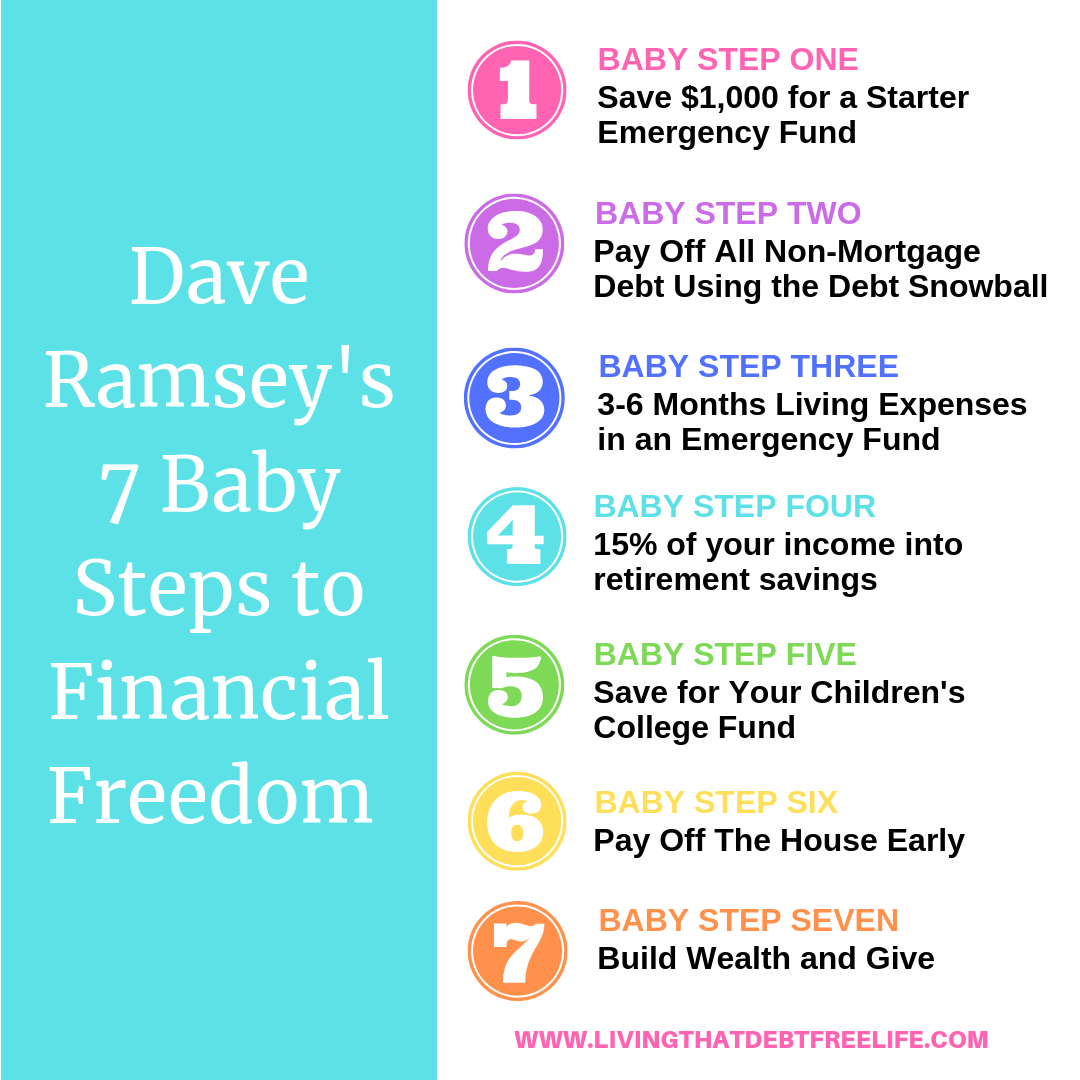

In this tutorial, we are focusing on non-mortgage debt only, in accordance with Dave Ramsey’s Baby Steps. Paying off the mortgage will come later, after you’ve gotten rid of consumer debt and beefed up your emergency fund. For those of you who aren’t familiar with the baby steps, check out this infographic:

Ok, back to paying off the debt!!

STEP ONE. List all your non-mortgage debt, by total balance owed, from smallest amount owed to largest amount owed. Don’t worry about interest rates. Just list the debts from smallest to largest. If you have two debts that are the same amount, then list the highest interest rate debt first. Otherwise, forget about interest rates for now. You may want to consider pulling your credit report to make sure you get everything! You can pull yours for free, once a year, here.

STEP TWO. Make a zero-based budget to determine how much extra money you can send to debt each month, above the minimums. That’s the amount of money you will use to begin your debt snowball. It doesn’t matter if it’s $100 or $10. Every little bit counts, and as you will see, the amount you send to any given debt will grow over time, as long as you just keep working the plan.

STEP THREE. Send minimum payments to all your debts.

STEP FOUR. Target the smallest debt on your list first. In addition to the minimum payment you sent to this debt in Step 3, send every extra penny you can find to this debt. Use your zero-based budget to help you figure out exactly how much you can send each month. (For a real glimpse into my zero-based budgets, head to the saved stores on my Instagram Page, under Budgets.)

STEP FIVE. Continue targeting the smallest debt, by sending in minimums plus every extra penny you can find until the smallest debt is paid off.

STEP SIX. When the smallest debt is paid off, take the full amount you were sending to that debt, (minimums + all the extra) and add it to the next debt on your list.

STEP SEVEN. Keep tackling debt, one at a time, with focused intensity, until all the debt is paid!

Example Debt Snowball

Let’s see how this debt snowball plays out, over time. Here’s an example of a debt snowball in action.

In the photograph above, you can see that the debts are arranged from smallest to largest, by total amount owed, completely ignoring minimum monthly payments and interest rate.

In the example above, the total outstanding balance of all debts is $28,840 with total monthly payments of $646. Making regular monthly payments, interest will cost $5,881.34 and you won’t be out of debt for 124 payments, or more than 10 years!

But, let’s assume, that after you complete your zero based budget, you have $354 extra each month to throw at the debt. Your total current monthly payments total $646, plus the additional amount of $354, is equal to $1,000. With this debt snowball, you will send $1,000 to your debts each month, until they are all paid off.

Here’s specifically how you would do it:

Begin by paying minimums each month of $646.

Send your $354 extra debt payment to Credit Card 1. That will result in a total monthly Credit Card 1 payment of $394 your first month. Keep throwing everything at Credit Card 1 until it’s paid. With this method, Credit Card 1 will be completely paid after 3 months, and you can move on to Credit Card 2.

After 9 payments, Credit Card 2 will be paid in full, and you can move on to the student loan.

The student loan will be paid off in 26 payments, and the car loan will be history in 32 payments.

With the debt snowball, you’ve completely paid off all your debt in less than 3 years! Wayyyy better than the 10+ years if you had just paid minimums.

And that doesn’t count any bonuses, or raises, or side hustles, or windfalls you may receive along the way!

Not to mention the interest savings! By paying only minimums, you’ll end up paying $5,881.34 in interest throughout the life of the loans.

But, with the debt snowball, you’ll pay only of $2,455.80 in interest throughout the life of the loans—a total overall savings of $3,425.54.

It’s almost as if someone is paying you $3,425.54 to get out of debt sooner!

Below is a screen shot of your debt snowball in action!

I had to split this into two pictures because I’m not that excel savvy.

(Information obtained from The Debt Snowball Calculator, courtesy of financialmentor.com. Calculator can be found at https://financialmentor.com/calculator). Play around with the calculator above to see how much faster you can get out of debt!

Get Started on Your Own Snowball!!

Get started with your own debt snowball today, by following the steps above. I promise, once you get rolling, you will wish you would have started sooner!

I wish you tons of luck as you start paying off debt. Know that it will be difficult and challenging at times, but every sacrifice you make will be 100% worth it, when you are completely debt free!

If you have any questions about the debt snowball, leave them in the comments below!!